It all boils down to Risk, Return and Liquidity | Demystifying the world of financial assets

I learnt from a small investment loss what some of the largest banks in the US learnt after losing their business.

It was July of 2021 when my banker persuaded me to invest my savings in a government bond. He had me successfully convinced to view them as a higher return, highly liquid and risk free investment opportunity. Fast forward 18 months and I learnt an important lesson about investing by losing money in a product that was supposed to be risk-free. This is not the story of a scam or a duplicitous marketing ploy played on me by a bank but a sub-optimal financial decision on my part.

Almost 2 years later in May 2023, I feel a lot better that I got to learn this valuable lesson a lot more cheaply than the now failed 14th and 16th largest banks in the United States.

I hope that sharing this personal incident with you will help you better understand the concepts of return, risk and liquidity and how to evaluate financial assets or investment opportunities across these three broad dimensions. These three dimensions are going to the foundational units of analysis in this series of posts around building wealth via savings.

So here goes my story

The initial investment

I had gone to the bank for an unrelated matter relating to my account when the banker looked at my profile on the bank’s systems. He saw that I had a fairly significant sum of money in my savings account and pitched me to invest it in a government bond. He proposed that I could invest my money to get a sliver of a 5-year Government of Pakistan government, issued in October 2020 and carrying a 7% annual coupon paid biannually.

I majored in economics in college; graduating in 2015. I had taken several courses in finance, investments and macroeconomics and had a fair understanding of how bonds worked and what the risks are, in theory. However, six years later, my decision analysis was a lot more rudimentary than the complicated bond pricing and valuations models taught in class.

I reasoned that:

The 7% coupon was higher than the 5.5% interest rate offered on the savings account at the time. So relative to the savings account the bond did seem to be the better option for earning a higher return as the banker suggested.

The sovereign bond, denominated in the local currency, is virtually free of default risk. The sovereign government can always print more money to pay back the bond. This may even be safer than the savings account in the bank, since any deposit in the bank, beyond the deposit insurance limit, is at risk of loss if the bank goes bust. The bank is much more likely to fail than the sovereign government.

The money invested in the government bond wasn’t as liquid as money in the bank, yet the bond could be sold for cash within 2-3 working days, making the government bond fairly liquid.

Therefore, primarily due to the higher return, I opted to directly invest money in the government bond which seemed a much better option than keeping it in the bank savings account.

What happened next…

I had purchased the slice of the government bond in July 2021 and held onto it in my investment account at the bank.

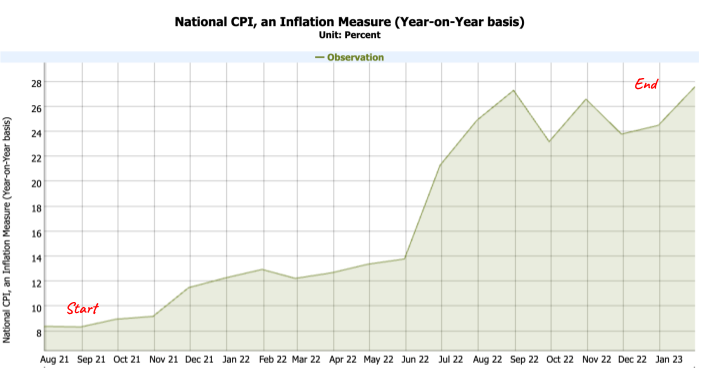

This was the time when interest rates and inflation in Pakistan were at the lowest during the past five years. From that point onwards, inflation in Pakistan started picking up sharply from around 8.5% in Aug 2021 to almost 28% by Jan 2023.

The central bank (State Bank of Pakistan) followed suit by hiking interest rates from 7.5% in July 2021 to 17% in Jan 2023.

The way bonds work is that an issuer (in this case the Government of Pakistan), issues a bond to borrow money on a particular issue date (15th October 2020). The bond matures after a certain time period (5 years), at which point the issuer will pay back the face-value of the bond. Over the course of the 5-year period, the issuer may also periodically make coupon payments at the annual coupon rate (7% paid out bi-annually).

When the issuer first issues a bond, with a face-value and coupon rate, the capital markets value the bond offering to come to the price that the issuer will get on the issue date in exchange of returning the face-value on the maturity date and coupon payments over time.

During the course of the term of the bond, the lender / the individual or institution that invested in the bond, can also sell the bond in the secondary capital markets to another party at the trading price of that day. The particular trading price varies with each day and is primarily a function of central bank interest rates, inflation expectations and the risk of the borrower defaulting on the loan.

Back to my story, to recap, the bond I invested in was issued by the government on the 15th of October 2020 for a 5-year term, maturing on 15th October 2025. It carried a coupon rate of 7% to be paid out twice a year in May and October.

It was the bank that actually sold the bond to me in July 2021. If the face-value was 1000, the trading price in the secondary market when I bought the bond from the bank was 986.

Overtime, as inflation in Pakistan began to sharply rise with interest rates following suit, the secondary market trading price of the bond began dropping sharply. As a rule of thumb, bond prices are almost always inversely proportional to interest rates and inflation expectations. My bank did notify me of this through monthly account statements that mentioned the mark-to-market valuations of my investment account. However, I did not take any action and let the bond continue its journey towards maturity.

Liquidation

Come January 2023 and I had a major life event with associated large expenses coming up that I hadn’t foreseen when buying the bond; home renovations and my wedding. I tried but the caterers and contractors refused to accept the sliver of the government bond as a form of payment and so I had to ask my bank to liquidate my investment in the government bond i.e. sell it for cash.

I bought the bond from the bank during July 2021 for 986. If I had held on to it till October 2025 (till maturity), I would have gotten back the face-value of 1000. However, since I had to liquidate the bond early to meet the large personal expense in January 2023, when central bank interest rates were at 17% as compared to 7.5% when I first bought the bond. The prevailing trading price for the bond I got at the time of sale was 780.

I lost 21% of the capital value of the bond between July 2021 and January 2023 due to the early liquidation.

I did get coupon payments at the annual coupon rate of 7% thrice during the time I held the bond. I put the coupon payments in the savings account at the bank. Over the 18-month period between July 2021 and Jan 2023, I got a total return of 11.4% over my initial investment from the reinvested coupon payments. However, because of the rising interest rates, If I had kept the same capital in the savings account at the bank, I would have gotten a return of 16.1%.

So in total, over the 18-month period, I made a loss of 25.7%, 21% in nominal capital loss and 4.7% from the net opportunity cost of profits that I could have earned from keeping the money in the bank savings account.

This doesn’t sound too terrible, so how can it cause a bank to fail

Let’s say for the 986 that I invested in the government bond in July 2021, only 36 was my personal capital and 950 was borrowed from a friend. My terms with the friend being that he could get back his full 950 any time he wanted. This could happen, but I considered a low probability of this happening and therefore proceeded with the deal.

Now let’s say in January 2023, it was the said friend that had the major life expense coming up. He asks for his 950 to be returned back to him so that he could meet the expenses. I would be in trouble since I could only give back 780 from selling the bond and 114 from the cumulative coupon paid out. If I had no other backup capital, I would not be able to give back the full 950 and would thus have to renege on the terms of my initial commitment and declare bankruptcy.

This is what happened in the US with Silicon Valley Bank and First Republic between March and April 2023. They had made investments into long-term US government bonds at a time when interest rates were at all-time lows. They failed to predict the increase in inflation rates between 2022 and 2023 and could not manage the outcome from the US Federal Reserve hiking interest rates in response. The interest rate hikes by the Federal Reserve led to a fall in the value of the US government bonds. When the depositors of these banks realized that the banks were sitting on huge losses on their holding of US government bonds, they got concerned whether the banks would be able to make their deposits whole or not. This led to a rapid erosion of trust in the particular two banks, causing the depositors to yank away their deposits and forced the US government to take over and sell the two banks at throwaway prices to other banks who could absorb the losses and make the depositors whole.

Generalizing from this story

We see the themes of Return, Risk and Liquidity all playing a role in the story. These are the 3 fundamental dimensions along which different financial assets or investment opportunities can be evaluated.

Returns

Without going into the complicated mathematics of measuring returns which can be a discussion for another time, for simplicity, Returns here can mean the profits or losses on the initial capital invested.

Returns can be of two types:

Cash returns: When an investment generates and returns cash flow. In the case of the investment in the government bond, the cash returns coming from the 7% coupon payments.

Capital returns: The profit or loss on the price or value of the asset. Capital returns can be realized or unrealized. In the case of the government bond, due to the fall in price from 986 to 780, I had a capital return of negative 21%.

If I hadn’t sold the government bond, this would only have been an unrealized loss and the number would have varied over time. It would even revert back to being a profit closer to the maturity date of the bond.

However, whenever I did sell the bond at the lower price, the capital loss was realized.

The main reason I chose to invest the government bond at the time was the 7% coupon rate being higher in cash return than the 5.5% interest rated offered by the bank. Since I planned to hold the bond to maturity, I didn’t expect any significant capital return over the 52-month holding period, when the price would move from 986 in July 2021 to 1000 in October 2025.

Risk

If you only consider the English language definition of risk i.e. risk being the exposure to or chance of loss or injury, you’d be put off from investing in financial assets. This definition is also not entirely true from a financial perspective. If you ask a finance professional, they’ll give you a technical definition of risk of financial assets around deviations from expected outcomes that is hard to intuitively get.

I’ll try to explain the general idea of the risk in the financial context in a manner that may be simplistic but is intended to provide you with an intuitive understanding.

The risk of a financial asset is the likelihood of the cash return and/or the capital return of the asset not being what you expect. Risk in finance isn’t always negative, Oftentimes the returns are higher than you expect and in these cases riskiness leads to positive outcomes.

In the case of the government bond, the apparent risks were as follows:

Credit risk: The risk that the borrower i.e. the issuer of the bond wouldn’t honor the terms of the agreement or be unable to make payments when they come due.

In the case of a sovereign government issuing a bond in their domestic currency, this is virtually negligible, purely because the government can simply choose to print more money than default on its debt. Hence why government bonds are considered very low risk.

Cash return risk: The chance that of the cash returns not being what you expected when making the investment.

The terms of the bond dictated that the issuer would always pay the coupon payments as per coupon rate times the face-value of the debt. At an absolute level, the value of the coupon payment was expected to be exactly as stated since the government was unlikely to default.

Capital risk: The value of your capital going up or down.

This again being negligible since it was highly likely that the government will pay back the exact stated face-value of the bond upon maturity.

The hidden risks that I failed to see at the time of making the investment:

Cash return relative to a benchmark return: The absolute value of the cash return was highly likely to be consistent since these were dictated by the terms of the bond. However the cash return relative to a benchmark carried more risk purely due to the change in the benchmark.

In our case, the coupon payments were highly consistent but when compared to interest provided on savings in a bank, the coupon payments progressively became the worse option since the benchmark interest provided on savings accounts increased sharply as the central bank increased the interest rates.

Capital value at the market valuation: If I could have held the bond till maturity in October 2025, the market trading price of the bond would not have been relevant to me. I could be completely oblivious to the risk of inflation and interest rates moving up or down. However, since I had to pre-maturely sell the bond, I was suddenly exposed to the market, and all the interest rate rises over the past months hit to cause the large capital loss.

In the context of bonds, this is called the interest rate risk and duration risk. The effects of interest rates changing are most pronounced on longer-term bonds. If I would have known beforehand at the time of making the initial investment that I would need the cash back 18-months later, I would not have invested in a bond maturing in October 2025 and may instead have chosen a bond maturing closer to January 2023.

Side-note: You’d be justified in challenging my initial statement by saying that even if one does plan on holding the bond till maturity, the interest rates and market price are still relevant to them because they could form an updated expectation on the future interest rates and based on this reevaluate the entire investment thesis and if needed, choose to sell the bond prematurely and invest the money elsewhere. However, we are not going into that level of sophistication yet.

Liquidity

Cash is the ultimate asset when it comes to serving a means of exchanging value. Virtually everyone in a modern economy is ready give or accept cash, either paper or electronic, to buy or sell something,

Liquidity for financial assets means, how close they are with respect to cash, to serve as a medium of exchange of value. If not directly exchangeable, how easily and cheaply can they be converted to cash.

Money in a savings account at the bank, especially if it comes with a debit card, is virtually as liquid as money in a checking account. If there’s a high rate of acceptance of payment cards and bank transfers in the economy, then money in the bank is virtually as liquid as notes and coins.

For government bonds, they are not as liquid as cash since shops or service companies won’t accept them in exchange for goods and services. However, government bonds can be easily and cheaply sold for cash via a financial institution within a few working days. Therefore they are considered fairly liquid if not as liquid as cash.

Some examples of financial assets that are relatively illiquid are:

Real estate, it can’t be easily converted to cash. It takes time to be sold and has high transaction costs such as agent fees.

Equity in private companies, these companies aren’t listed on a stock exchange, shares in these companies are hard to sell for cash.

Private debt, If you’ve lent money to your friend or your local small business, and you can’t recall the debt i.e. ask your friend or local business to give you back the money before it is due, It is also extremely hard to sell that debt to another party for cash. Thus as opposed to lending to governments or large-companies whose bonds are actively traded, privately lending to individuals or small businesses is highly illiquid.

Conclusion

I hope you now have a fair understanding of what return, risk and liquidity mean in the context of financial assets

You’ll often see strong correlations between them. Assets with high returns offered are often high risk and less liquid, Low-risk, liquid assets are almost always low-return. If you’re ever promised a high-return, highly liquid asset at low-risk, always be mindful of risk that may not be apparent but still lurks beneath the layers.

In the next post in this series, as we did with government bonds here, we dive deeper to evaluate other common financial assets such as Bank Products, Real Estate, Commodities, Equities, Debt, Mutual Funds, Hedge Funds, Cryptocurrencies along the dimensions of return, risk and liquidity.

Thought Provoking, Keep up the great work !